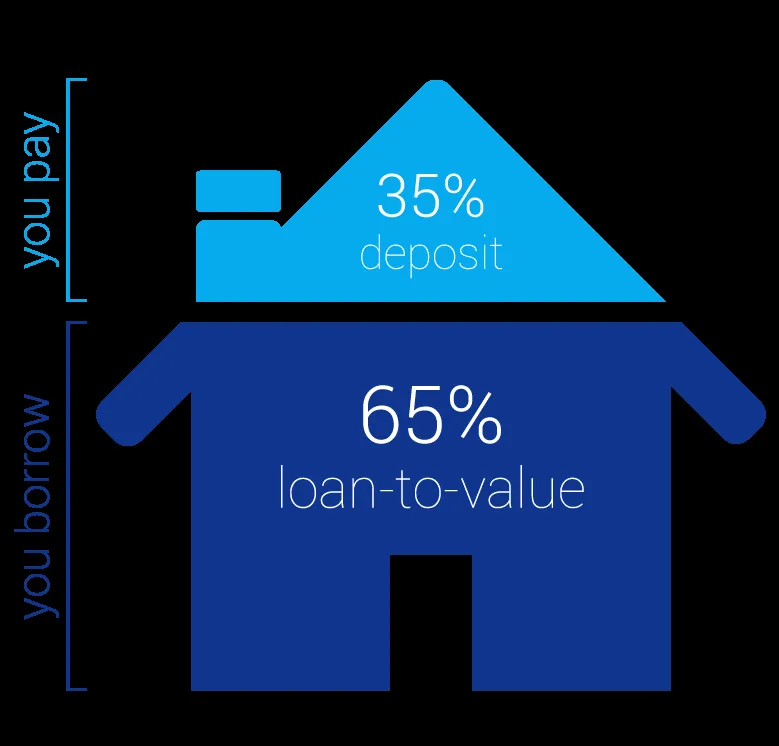

In a notable development for the UK housing market, sales of 100% mortgages have surged to a five-year high, with 574 transactions recorded in the first three quarters of 2025. This marks a significant increase from the 452 sales seen in 2021 and a stark contrast to the mere 135 sales in 2022, indicating a potential shift in buyer sentiment and market dynamics.

The rise in zero-deposit mortgages is symptomatic of a market in which many buyers are finding it increasingly difficult to save, according to Charlie Evans, a spokesperson for the Financial Conduct Authority. This trend is particularly pronounced in regions like the North West and South West, which reported the highest volumes of sales during this period.

As the average property price across the UK stands at £270,000 in December 2025, the implications of these mortgage trends are significant. England recorded an annual growth of 1.7%, bringing the average price to £292,000, while Wales saw a 5.0% increase to £215,000. In Northern Ireland, prices surged by 7.5%, reaching an average of £196,000.

Despite the uptick in mortgage sales, the market is not without its challenges. Mortgage approvals for house purchases fell by 3,100 to 61,000 in November 2025, suggesting that while some buyers are taking advantage of 100% mortgages, overall demand may be fluctuating.

The weighted average interest rate on new fixed-term mortgages currently stands at 3.46 percent. Borrowers could potentially save about €1,000 per year with a 0.5 percentage point differential on a €250,000 mortgage, highlighting the importance of timing in mortgage decisions.

Trevor Grant, a mortgage advisor, advises borrowers with fixed rates maturing in 2026 not to wait until their terms expire, indicating a sense of urgency in the current market. Rachel McGovern echoed this sentiment, stating, “It is a difficult one to call,” reflecting the uncertainty that many buyers face.

Overall, the surge in 100% mortgage sales raises questions about the sustainability of this trend and its impact on the broader housing market. As buyers navigate these changes, the responses from financial institutions and regulatory bodies will be crucial in shaping the future landscape of home ownership in the UK.